Assets. They have long complicated music industry economics.

Record companies have argued that they deserve to own the majority of sound

recording copyrights because a minority of artists succeed. They need to keep

the copyrights of the 10% of artists who recoup their advances in order to pay

off the losses of the 90% who are in debt. While the losses from ‘unsuccessful’ artists

are detailed in record company balance sheets, the value of their copyright

catalogues does not appear there. Nevertheless, as the Music Managers’ Forum

has argued, ‘the copyright catalogues of the record companies are their most

valuable asset’. Traditionally, the biggest deals that have been made in the

business have arisen when these catalogues have been sold on to other

companies. These transactions have happened when the major companies have

merged with one another and when larger companies have bought up indie labels.

Derek Green, head of China Records, made the economics of the indie sector

clear:

Well,

the only reason we do it is because on our balance sheets we have the value of

our masters and the value of our contracts marked as zero. Therefore

technically every year our accountants tell us we’re bankrupt. But what we

really know and believe is that the majors will pay millions to buy us.

The crucial factor about these takeovers is that the money went to

the owners of the record companies that were being sold. Unless artists

happened to have equity in the company, they would gain little, nothing or

perhaps even lose out from the sale. There are many stories of artists who

found themselves marginalised when transferred to a new corporation.

The sale of one record company to

another did at least have a degree of honesty and transparency about it. The

owner of the record company that was being sold would be profiting from an

institution that he or she had overseen. The assets up for sale were the

recordings that they had invested in, even if some of those recordings had been

fully subsidised by artists who had recouped.

Streaming provides continuities

and discrepancies with this model. We still have the situation whereby

companies are making little profit – even Spotify is running at a loss. The low sums of

money being generated by these companies is presenting a problem for record

labels, whose income from streaming is, in the first instance, based on a share

of advertising and subscription revenues. The record companies’ songs might be

being streamed billions of times, but this doesn’t mean that advertisers are

willing to invest in these new advertising platforms or that consumers are

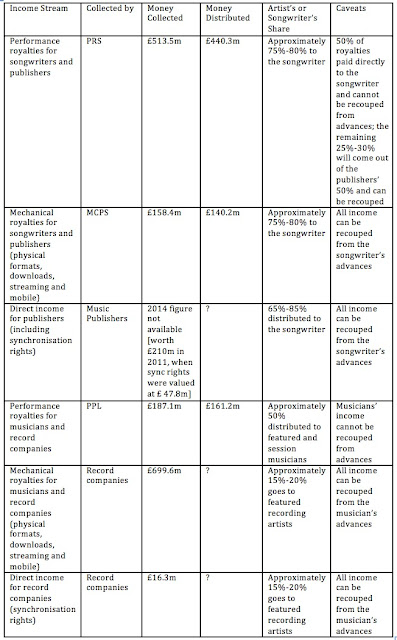

willing to upgrade to subscription services. Last year in the UK there were

14.8 billion individual audio streams and 14.3 billion video streams. Despite

this vast traffic, the money generated by subscription services only

constituted 12.4% of the total income for recorded music, while the money from

ad-supported services - although it was the avenue for the vast majority of those

29 billion streams - only constituted 3.5% of the same market. In total, the

income from streaming contributed £115m to the UK’s recording ‘sales’ last

year. Vinyl albums and CDs, meanwhile, contributed £320m. Record companies are

nevertheless continuing to have faith in streaming services. If the income

generated by these services hasn’t managed to offset the decline in physical

and download sales, streaming is having the effect of converting

‘pirate’ users of musical content into legal consumers.

What is more significant for our

immediate purposes is that record companies have found diverse ways to generate

income from streams. Their share of advertising and subscription revenue is

backed up by minimum guarantees. Each record company who enters into a

licensing agreement with a streaming company will be guaranteed a minimum sum

each time one of their tracks is played. In addition, some record companies

receive a guaranteed sum for each subscriber who signs up to the streaming

company. These minimums only come into force if the revenue target is not

reached. In the instances where this income did come into play last year, it

will have been reported as part of the total streaming income of £115m.

There are, however, areas of

streaming income that are not reported on the record industry’s balance sheets.

Most importantly, record companies demand equity in streaming companies as part

of their licensing agreements. Here, as the

MMF have identified, there is an echo of the ‘bankrupt’ nature of indie

record companies. Just as those old indie companies were aware that their

impoverished balance sheets disguised the fact they could be worth millions if

sold on to larger record companies, today’s record labels are aware that, when

it comes to streaming, the ‘single biggest revenue generator may be the sale of the streaming

business, either to an existing major tech or media firm or through flotation

on a stock exchange’. What is more, the record labels might even ‘agree to less

favourable terms on revenue share and minimum guarantees, where income is

shared with the artists, in return for a better deal on equity’. And who will get the money from

the sale of the sale of the streaming companies? The MMF have reported that:

The assumption is that many labels will

keep these profits in their entirety, citing clauses in artist contracts that

say the record company is only obliged to pay royalties to artists on income

directly and identifiably attributable to a specific recording.

Here there is a difference to earlier practice. The

record companies will be profiting from the sale of companies that they haven’t

even had a hand in creating. The labels might argue that they have provided the

essential content that has transformed streaming companies into valuable

commodities, but that content is sound recordings, which have been created and

in some cases paid for by recording artists. The record companies will not even

be selling this content on to the new purchaser of the streaming company: the

purchasing corporation will still have to licence the recordings. No wonder

then that it is artists, rather than record companies, who are raising

questions about the land of streams.